In the next step, chlorine is added to the water. This substance is responsible for eliminating microorganisms in the water that are prejudicial to health, making the water suitable for consumption.

Aegea’s consolidated net revenue in 2015 totaled BRL795.1 million, with variation of 32.6% compared to BRL599.5 million in 2014. This result reflects the 9.5% increase in the customer base: 13.2% in billed volume for the year.

Costs and expenses

If the effect of amortization is not considered, the Company’s costs and expenses were 28.9% higher, which is BRL87.9 million more than in 2014.

This total can be explained by the higher rates charged by power companies and by the fiscal crisis which impacted the ability of public agencies to make payment. Despite these impacts, growth in total costs and expenses was less than revenue growth, showing gains in productivity.

Costs and expenses (BRL thousands)

2014

2015

Personnel

114,411

132,148

Outside services

50,760

54,373

Conservation and maintenance

7,041

8,976

Materials, equipment and vehicles

18,260

19,891

Cost of concession

5,626

16,584

Electricity

46,629

86,909

Chemical products

4,296

5,884

Travel and lodging

5,224

4,792

Provision for doubtful debts

6,405

29,481

Provisions for contingency

157

(5,133)

Research and development of new business (R&D)

17,924

9,013

Other costs

27,842

29,603

Subtotal

304,576

392,522

Amortization

56,157

88,315

Total

360,733

480,837

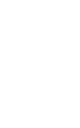

Energy costs grew significantly during the year, by around 86.4%. Of this amount, 14.6% is attributed to new companies and 71.8% to existing concessionaires, such as Águas Guariroba and Prolagos, due to an extraordinary price readjustment made by Brazil’s National Electric Energy Agency (Aneel), and to Águas de Matão, which achieved universal coverage of the concession area.

In relation to personnel costs, the staff at existing concessionaires was 4.6% smaller, with 105 fewer workers than the previous year. The result shows process improvements and more operational efficiency, especially with the expansion of Aegea Academy (learn more), aimed at enhancing skills at the strategic, tactical and operational levels and assure application of the Company’s Values in every phase of concession maturity.

Default

The 180-day default rate was 1.1% higher year-over-year in 2015. This increase can be credited to the government consumption category, which had higher share percentages in default, going from 14.9% in 2014 to 30.5% in 2015. Moreover, Aegea has monitored the national economic scenario, particularly numbers on jobs, earnings and consumer buying power and its impacts on its users’ capacity to make payment, especially its government customers. In order to bring these numbers down, the Company has intensified campaigns to encourage renegotiations of accounts past due, up by 16% year-over-year, and enrollment in automatic bill pay.

Operating income and Ebitda

Consolidated operating income for the year was BRL314 million, which represents year-over-year growth of 31.6%. Ebitda totaled BRL402 million, 36.5% higher than in 2014. This result was due to gains in efficiency, which contributed to lower personnel costs (see Costs and expenses).

Ebitda (BRL thousands)

2014

2015

Operating income

238.778

314.289

(+) Depreciation and amortization

56.157

88.315

Ebitda

294,935

402,604

Ebitda margin (%)

49.2

50.6

Net earnings

Aegea’s net earnings in 2015 were BRL115.156 million, a 2.6% increase compared to the previous year. This performance shows the ratio between the increased customer base and lower operating expenses. It was not more elastic due to an increase in the cost of electricity that was above the Company’s projections.

Cash flow

Cash flow from statement (BRL THOUSANDS)

Cash flow from operating activities

2013

2014

2015

Earnings before taxes

69,015

50,813

(34,471)

Adjustments for:

Amortization and depreciation

47

2,132

2,162

Interest on loans, financing and debentures

27,900

32,384

25,122

Fair value adjustments to loans and financing

0

0

5,662

Exchange rate loss

0

0

41,898

Derivatives

0

0

(34,869)

Interest on financial investments

(15,009)

(23,537)

(23,560)

Result of equity accounting

(132,339)

(130,626)

(147,968)

Changes in assets and liabilities (Increase)/Decrease of assets

Customer accounts receivable

(26,216)

(58,659)

(58,203)

Inventories

(2,622)

934

(1,558)

Current and noncurrent fiscal assets

12,166

(17,130)

(12,222)

Advances to suppliers

0

(4,729)

(7,640)

Other credits

(10,284)

(843)

(20,383)

Increase/(Decrease) of liabilities

Suppliers and contractors

(5,806)

31,287

16,590

Labor and social obligations

2,571

8,912

6,082

Tax obligations

(2,857)

8,080

(3,223)

Tax payments

(3,148)

(1,661)

452

Payment of contingencies

(129)

(500)

(4,080)

Other accounts payable

(70,547)

1,963

(18,292)

Interest paid

(76,822)

(98,487)

(131,274)

Income tax and social contribution paid

(48,179)

(43,842)

(72,197)

Cash flows from investment activities

Financial investments and debentures

(273,352)

48,716

191,932

Dividends and interest received on shareholders’ equity

0

1,000

1,570

Investment losses

0

173

0

Acquisition of fixed assets

(14,030)

(8,566)

(3,177)

Acquisition of intangible assets

(175,848)

(386,822)

(338,668)

Advance for acquisition of business

0

(12,500)

0

Acquisition of the Agência Ambiental controlled

company, net cash obtained in the acquisition

0

(29,788)

0

Cash flows from financing activities

Loans, financing and debentures raised

185,067

7,000

150,000

Loans, financing and debentures paid

(185,585)

(350)

157,936

Current accounts receivable from related parties

(26,087)

(41,536)

(70,352)

Dividends paid

(86,000)

(86,000)

(123,820)

Capital investments by minority shareholders

in controlled companies

287,775

0

0

Net increase (decrease) in cash and cash equivalents

(14,908)

(3,894)

5,012

Initial Balance of Cash and Cash Equivalents

18,933

4,025

131

Final Balance of Cash and Cash Equivalents

4,025

131

5,143

Indebtedness

The balance of cash and cash equivalents and short and long-term financial investments ended the year at a total of BRL395.8 million. Gross debt (including hedging) for the same period was BRL1.6 billion.

Indebtedness (BRL thousands)

2014

2015

(%)

Ebitda

294,935

402,604

36.5

Net debt

815,756

1,170,578

43.5

(+) Gross debt (including hedging)

1,343,463

1,566,361

16.6

(-) Cash

(527,707)

(395,783)

-25.0

Net debt/Ebitda

2.77

2.91

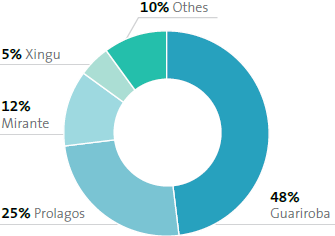

Reduced cash flow is the result of an accelerated curve of capital expenses (CAPEX), the outcome of which is a lower financial yield than in 2014.

CAPEX BRL millions

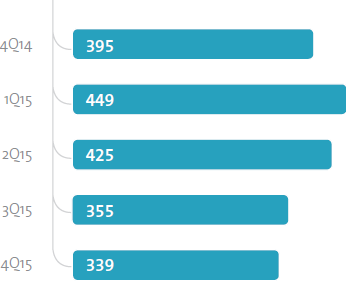

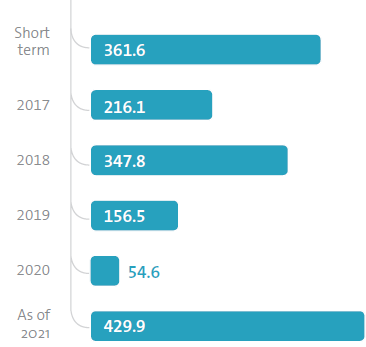

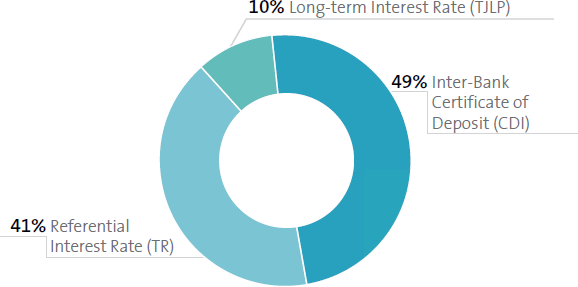

Debt distribution profile

Timeline of amortization of debts (BRL millions) – Others