In 2013, QGEP promoted another edition of the materiality test, in order to build a new matrix of topics material to management and the sustainability report. The Company had already carried out this process in 2011, which served to direct actions and accountability for that year and the following period.

QGEP also used compliance with principles as the basis for defining the report’s content – which are inclusion of stakeholders, context of sustainability, materiality and completeness – to identify material impacts and aspects. All QGEP stakeholders were invited to participate in the consultation (local community, civil society, clients, shareholders, capital providers, suppliers, employees, trade associations and government agencies). Application of the test was done at two onsite events, in Rio de Janeiro and in Bahia, and via an online questionnaire.

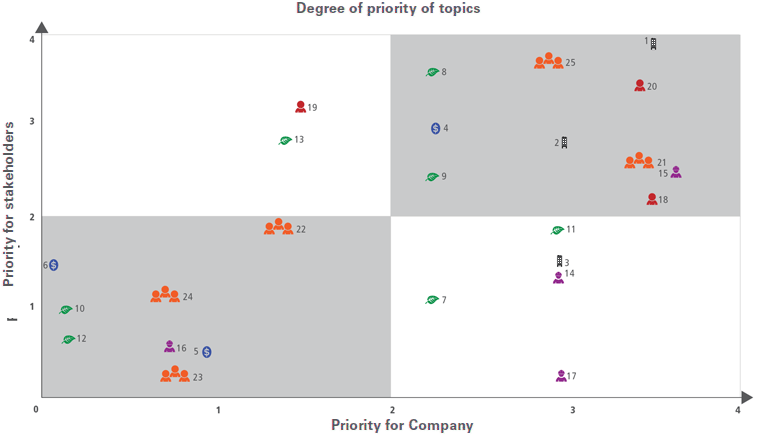

GRI G4-24G4-25One-hundred responses from stakeholders were consolidated, forming the Y axis of the matrix, and four responses from Executive Board members, forming the X axis, as shown on the table. Individual assessments were tabulated by public, determining the average for each of the topics for all stakeholders. Based on a cross-referencing of averages for stakeholders and averages for the QGEP upper management, a materiality matrix was created, as shown in the graph.

| PUBLICS CONSULTED (104) | |

|---|---|

| X AXIS | |

| Upper Management (4) | |

| Eixo Y | |

| Academia (6) | Supplier (23) |

| Shareholder (3) | Press (5) |

| Analyst/Investor (5) | Regulatory agency (1) |

| Employee (22) | Partner (14) |

| Community (16) | Civil society (5) |

The matrix is split into four quadrants: green gathers topics of extremely high relevance (priorities for stakeholders as well as for upper management); yellow quadrants contain highly relevant topics (for stakeholders, in the top left corner, and for the Company, in the bottom right corner); the white quadrant contains low relevance topics.

While carrying out consultations, various topics and concerns were raised by the stakeholders consulted – such as concern with local community rights, appreciation of diversity, relations with public agencies, etc. These matters are inputs for enhancement of the methodology for future consultations.

GRI G4-27Considering the G4 version of the GRI guidelines and the level of maturity of the reporting process, QGEP chose to draft its report with a focus on the material topics identified by the test, including those of extremely high or high relevance, since those in the high relevance quadrants had topics connected to the Company’s strategy and are considered important in terms of accountability.

GRI G4-48Ten topics were considered to be of extremely high relevance:

GRI G4-19All material impacts and aspects occurred inside and outside the Company. Although aspects 18 (Human rights practices) and 20 (Child and compulsory labor) are material, they are not recurring issues, since the oil and gas sector is extremely regulated. Although aspect number 25 (Health and safety of customers using products) is material, it does not provide results, due to the fact that QGEP has still not reached the production stages in the blocks were it operates.

GRI G4-18 | G4-20G4-21G4-HR11Global Compact 2