Capitals: Financial, Social, Human, Intellectual, Manufactured e Natural

StakeholdersCLPIAIFGCO

Interested Parts: Clients, Employees, Shareholdres and Investors, Suppliers, Government (Regulatory Authorities) and Community/Society/Third Sector

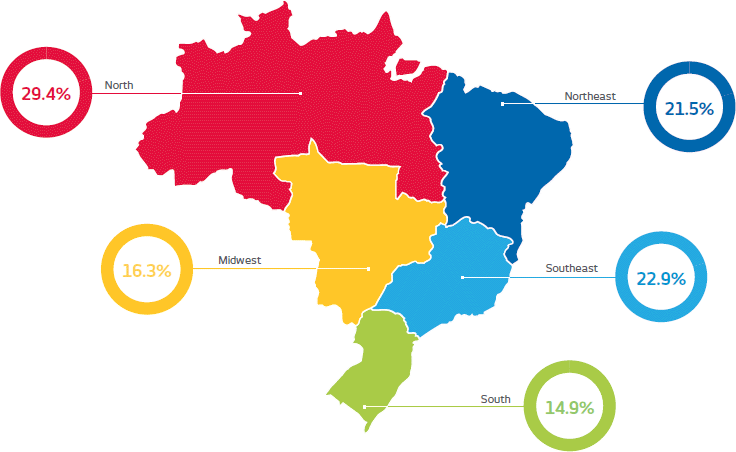

Bradesco generates value for its stakeholders offering a combination of banking and insurance operations in every municipality in Brazil

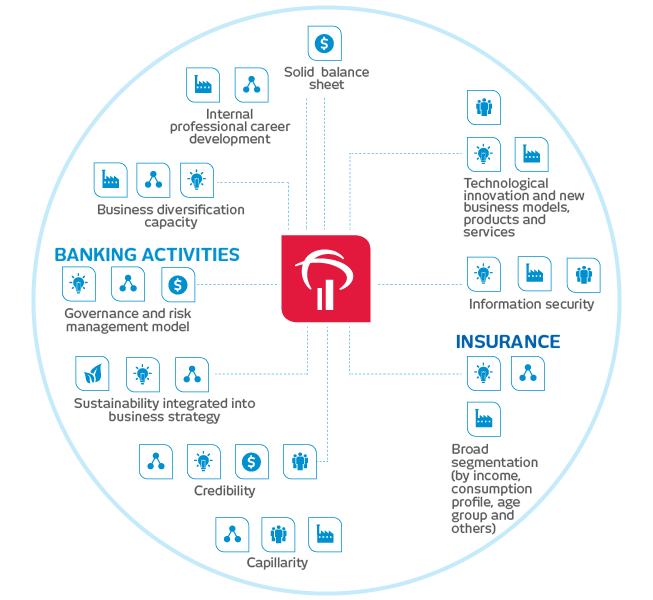

Business model

Bradesco strategy is based on a balanced business model which combines banking and insurance activities and the Organization’s presence in all the municipalities in Brazil – serving all social classes through its segmented structure and various options of digital and physical access. The inputs and key elements of the strategy which generates value for Bradesco are presented in the infograph bellow.

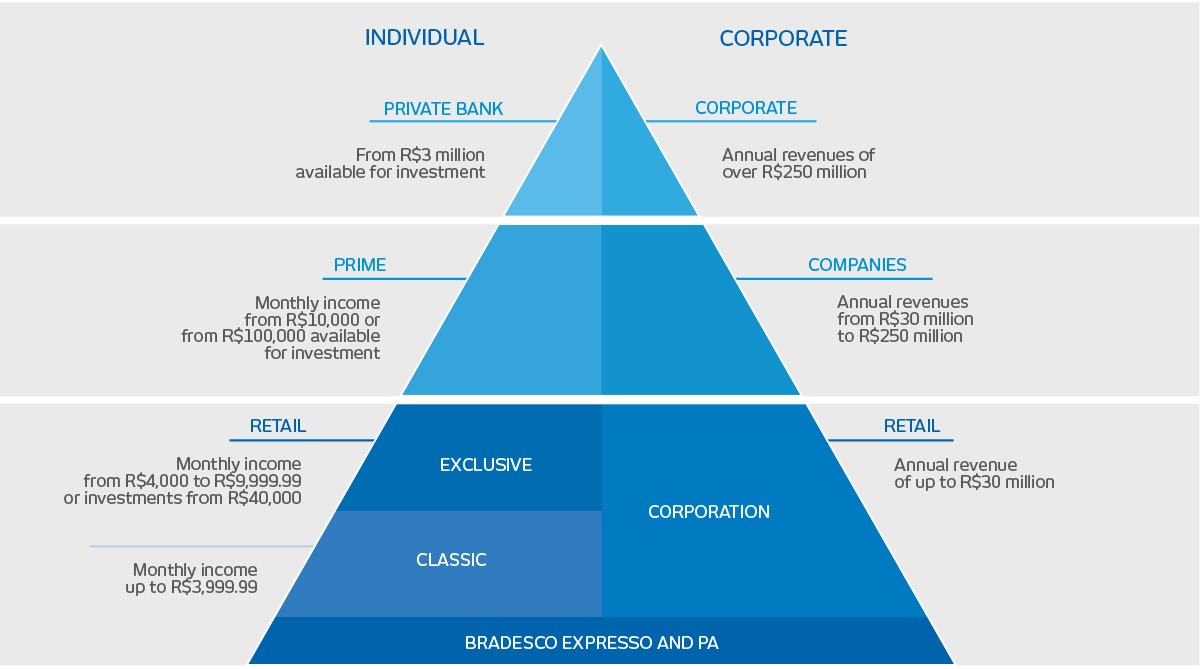

With client relationship-oriented measures, the segmentation process at Bradesco is aligned with the market trend towards grouping consumers with the same profile together, permitting differentiated service and greater speed and productivity. This process enables greater flexibility and competitiveness in the execution of business strategy, generating scale in operations for both individuals and corporations, driving quality and specialization and meeting the specific requirements of the most diverse client groups.

Segmentation is based on four basic factors: client income, amounts invested, behavior towards the Organization and profile. These criteria are used to determine service network expansion measures to promote new opportunities for financial inclusion.

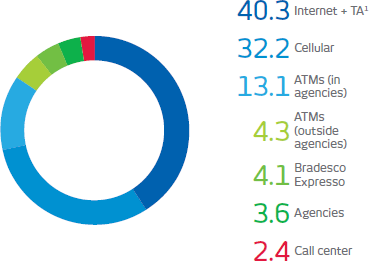

An example of this was the observation that 2.4 million account holders had not been to a bank branch in over three months, prioritizing relationship exclusively via electronic media, such as the internet, mobile phone or ATM. This client universe conducts 92% of its transactions via digital channels.

Social inclusion, accessibility and quality of life (nationwide presence, bankarization and customized means of access; development of culture focused on provision of economic security and financial provision for people)

The client universe familiarized with and using digital channels resulted in a 26% reduction in transaction volume with tellers at branches in 2015, representing more than 10.5 billion operations conducted exclusively through digital channels and no longer using physical channels. At the end of 2015, 32.2% of client transactions were conducted via cellular telephone, showing how engaged the consumer is in this easy, safe and readily available technology. This also strengthens the bank’s focus on preparing for the digital era, opening up new possibilities and generating benefits for clients, in addition to enabling Bradesco to develop a cost structure appropriate for serving its diverse client groups.

Comparison of Weighted Average Costs by Channel1, 2 (%)

The segmentation model also benefits commercial clients through the reformulation and launch of the application Bradesco Net Empresa for cell phones. An exclusive Bradesco novelty in the new version is the inclusion of service enabling users to deposit checks via a smartphone camera. This solution modifies the process of capturing, storing and depositing the check, meaning that both individual and corporate clients no longer need to physically make the deposit at a branch or at an ATM. The application also enables consultations and financial transactions, such as payments, transfers, loans, deposits, working capital finance or overdraft facilities.

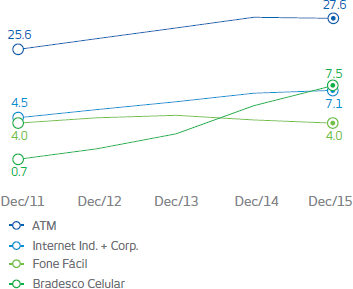

Relationship channels – active users per digital channel (millions of users)

11% of our clients are exclusively digital

electronic self-service channels gain popularity (%)

Electronic and digital platforms account for 92% of bank transactions

During the year, the Organization also undertook the segmentation of its portfolio of Bradesco Net Empresa corporate clients, with differentiated products and services for the client profile whose revenue exceeds R$3.6 million per year. One thousand managers were allocated to provide exclusive service for this group.

As a result of its strategy, the Organization ended 2015 with an Operating Efficiency Ratio of 37.5%, its best ever. This indicator, which measures the ratio between operating expenses and operating revenues, demonstrates how Bradesco generates value.

Brand management

Its capacity to meet the needs of clients at different social and economic levels, the capillarity of the service network, its open door culture, its governance model, robust results, open approach to credit concession and bankarization are some of the factors that add value to the Bradesco brand, one of the Organization’s main intangible assets.

Brand management is the responsibility of the Marketing area, which tracks the annual Valor da Marca (Brand Equity) study for each of Bradesco’s market segments, monitoring the indicators that impact this value.

The area uses certain management instruments to do this, including the Brand Control by Segment and Brand Assessment Panels. Moreover, the Organization also monitors its communication actions and Olympic sponsorship via specific control panels. There is also the Monthly KPI (key performance indicator) Panel, with inputs from a national survey that monitors the relationship between the brand and competitors in the short term.

According to the surveys conducted in 2015, the Bradesco brand has one of the highest recall rates and continues to dispute leadership in Market share, Main Bank and Recommendation with its major competitors in the Individual segment. In the High Income segment, Bradesco Prime is distinguished by its high levels of Satisfaction and Recommendation among account holders. In the Commercial Retail segment, Bradesco improved in Brand recall and in Recommendation and Preference.

With 68 million clients, including 26 million account holders and 50 million Bradesco Seguros insurance policy holders, the Organization provides individual and corporate clients nationwide with segmented products and services such as checking and savings accounts, credit operations, issuance and management of credit cards, consortiums, payment receipt and processing, insurance, supplementary pension and capitalization bonds, investment banking, commercial leasing, asset management and intermediation services, in addition to securities brokerage services. G4-8

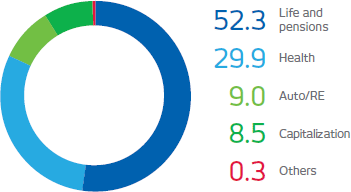

Bradesco was the leader in the Latin American insurance market in 2014. The company led the Brazilian market in 2015 with a 25.5% share in insurance premiums, supplementary pension contributions and capitalization bonds. The offer of mass market insurance is maintained via products with simplified contracts commercialized by the branches and other service points located in low-income regions. The best-selling product is Primeira Proteção Bradesco, with 4.08 million contracts signed since its launch in 2010.

Main indicators

2012

2013

2014

2015

Revenues from premiums, pension contributions and capitalization bonds (R$ b)

44.308

49.752

56.152

64.612

Total assets (R$ b)

154.371

161.016

182.402

210.207

Claims and benefits paid (R$ b)

26.394

33.771

38.546

45.272

Number of policy holders clients and participants (million)

Primeira Proteção Bradesco is outstanding, with more than 4 million contracts signed since 2010

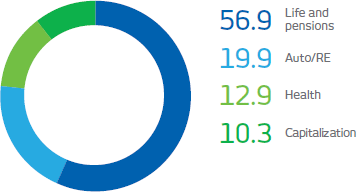

In 2015, Bradesco Seguros concluded the integration of the entire commercialization structure for its products and services, aimed at understanding clients better to drive service improvements and internal synergies. Previously each Bradesco insurance company commercialized specific types of insurance separately. Unification drove significant expansion in service capillarity, enabling the client to acquire total protection for all risks in a single place. This was made possible with diverse changes in the distribution model, with brokers selling different types of insurance through the branch network. In 2015, almost 2,700 brokers increased the number of types commercialized compared with 2014. The changes enabled great gains in productivity, with new sales for the Insurance Group growing 21% in 2015, worthy of note being Pensions (30%), Life (33%) and Health for Small and Midsize companies (47%).

In line with the models existing in the market and with the legislation in force, the Grupo Bradesco Seguros has an Actuarial Studies and Risk Management Department, with an operating structure specialized by type of risk and function, enabling an integrated vision and alignment with the Bradesco Organization risk management structure. To ensure uniformity in the risk management process, the Group has its Grupo Bradesco Seguros and BSP Empreendimentos Imobiliários Executive Risk Management Committee, which meets on a quarterly basis to approve strategies, standards and procedures.

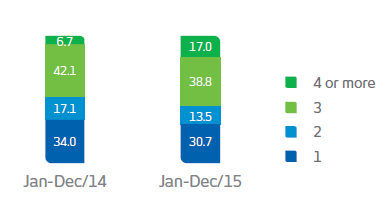

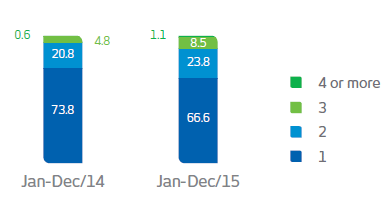

Breakdown of brokers by channels

Growth in number of types of insurance sold by the same broker

BROKERS IN THE NETWORK (%)

BROKERS IN THE MARKET (%)

Note: considering only new sales (redemptions, portfolio, renewals and cancellations were not taken into account). Types considered: Auto/RE/Bilhete, Pension, Life and Corporate Health/Dental.

Source: PGC production bases.

The Bradesco seguros risk management structure is aligned with the rest of the organization

In 2015, the company also concentrated its São Paulo state units in a single location in the city of Barueri, in Alphaville, the objective being to drive synergies in the internal areas and reduce costs. The new Bradesco Seguros headquarters were designed and built in accordance with the most rigorous Brazilian and international safety and sustainability standards, having LEED Gold for New Construction (Leadership in Energy and Environmental Design) pre-certification. This is granted by the US Green Building Council

(US-GBC), in accordance with rational resource use criteria (energy, water etc.).

Strategy to drive business sustainability

Bradesco strives to incorporate best sustainability practice into its businesses, taking into account the context and potential of each region, by integrating these concepts into its corporate strategy, using business risks and opportunities and organizational management as drivers.

Strategic sustainability-related goals were developed based on corporate directives such as ethics, innovation, efficiency and stakeholder relations. The Organization adopts the voluntary commitments to which it is a signatory and the criteria of sustainability indices (DJSI, ISE, among others) as guidelines for the initiatives to be implemented by the diverse areas over the next three years. In 2015, there was progress in the definition of the roles and responsibilities of these areas in enabling the implementation and the monitoring of the results of these projects.

Bradesco has a robust governance framework comprising committees, policies and standards that oversee the adoption of social and environmental responsibility guidelines in business and in stakeholder relations.

The Sustainability Committee supervises the effective implementation of the relevant guidelines, as well as aiding the Board of Directors in exercising its attributions related to fostering sustainability strategies.

The Corporate Sustainability Policy determines that sustainability be integrated into other company policies to ensure that relevant social and environmental impacts for the Organization be managed properly.

The policy was reviewed, taking into account the principles of relevance and proportionality set forth in Bacen Resolution No. 4,327. Another document supporting the implementation is the Social and Environmental Responsibility Standard, which establishes the main guidelines for business-related social and environmental actions and relations with Bradesco stakeholders, underscoring lines of action, governance, roles and responsibilities.

The Bradesco Organization makes its policies and practices available for the public on the website www.bradesco.com.br/ir, including the Corporate Sustainability Policy and the Social and Environmental Responsibility Standard

In 2015, social and environmental risk was incorporated into the risk governance framework and the Executive Operating and Social and Environmental Risk Standard was decided on by the Executive Operating and Social and Environmental Risk Management Committee, the purpose of which is to control the Organization’s exposure through the identification, assessment, classification and monitoring of both credit operations and supplier relations.

The document describes the scope of assessment and management of social and environmental risks adopted in the elaboration of reports supporting credit decisions, including indications of forced labor and activities in which there is greater exposure to social and environmental risk, such as arms production and trade, timber processing, activities using radioactive materials, among others. It also covers operations involving the production and commercialization of products or activities considered illegal under Brazilian law and international conventions and agreements (child labor, sexual exploitation, animal traffic, etc.). G4-14

Furthermore, the scope of the social and environmental risk standard encompasses the verification of contaminated and embargoed areas in credit operations or in suppliers, as well as the assessment of project financing.

As a signatory to the Equator Principles, in addition to the criteria and obligations established by Brazilian legislation, Bradesco requires the application of the Equator Principles guidelines, including the International Finance Corporation (IFC) performance standards and the World Bank health, safety and environment standards in any projects financed under the scope of the commitment, the risks being categorized as High (Category A), Medium (Category B) or Low (Category C).

For operations classified under the Equator Principles in categories A and B, the bank requests that the clients undertake impact studies to identify social and environmental issues. The social and environmental aspects are included in the contracts and considered in the action plans and are monitored until the finalization of the operation. In this context, interactions with clients regarding the assessment of social and environmental risks in projects are conducted by departments of the bank, other financial institutions and by specialized independent auditors.

At the project analysis phase, the client is informed of the Bradesco social and environmental risk management policies and practices that are applicable to the operation. Whenever necessary, documentation and information provided by the client is assessed and recommendations are made to improve and adapt the project in accordance with the Organization’s guidelines, legislation and IFC performance standards (when applicable). These procedures may result in the inclusion of specific social and/or environmental clauses and/or an action plan prepared jointly by the client and the bank, identifying any gaps and proposing time bound improvements. The bank informs the client when the monitoring process will be initiated, clarifying any doubts about the social and environmental criteria, arranging conference calls, meetings and visits to the project site, as well as tracking the progress of the action plan by means of periodic reports.

A series of internal meetings were held with analysts and managers to disseminate the new processes and procedures related to the Equator Principles III. To add value to the analysis and control of social and environmental risks and drive team development, the analysts also take part in meetings involving specific questions.